It’s hardly news to say that the price of owning a home in Canada has skyrocketed in recent years. What might be surprising, though, is just how unevenly this trend has played out across the country.

In most cities across Canada affordability has moved further and further out of reach. But one region stands out for its relative affordability: Alberta.

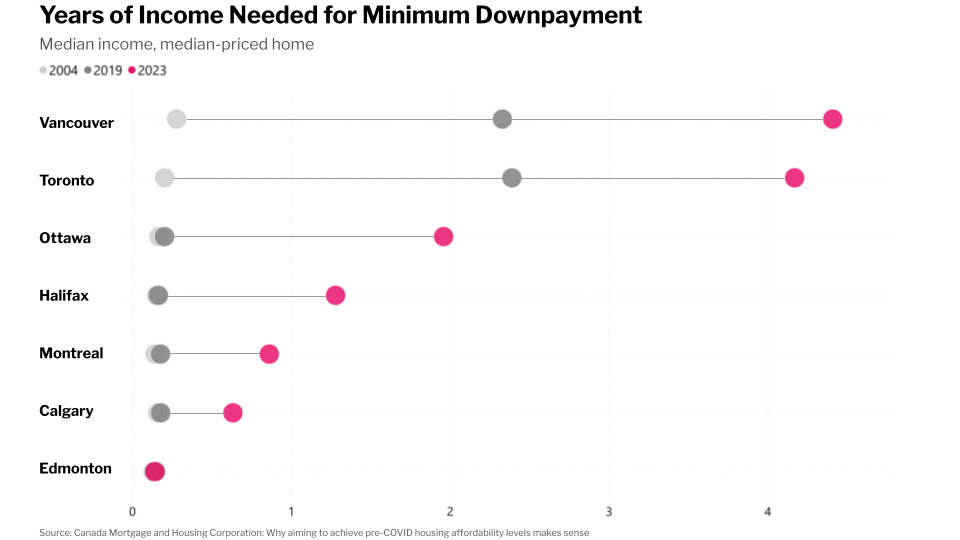

Historically, things were a lot more balanced than they are today. In 2004, if a typical worker wanted to make the minimum down payment on a typical home, it would cost about two months’ wages to do so. That was true in nearly every major Canadian city. Even in notoriously expensive Vancouver, a down payment would only set you back 3.5 months of pay.

Since then, however, housing affordability has deteriorated rapidly, especially in Canada’s biggest cities. By 2019, the median worker needed to save two years’ worth of income just to make the minimum down payment on a house in Toronto and Vancouver. By 2023, it had climbed to four years.

Other large markets in Canada saw little change in affordability between 2004 and 2019, but a rapid deterioration since. While nowhere near on the same scale as Vancouver and Toronto, Ottawa, Halifax and Montreal have all seen housing affordability erode significantly over the last few years.

But the story is different in Alberta.

In Edmonton, it remains as affordable as ever to buy a home. A minimum down payment in 2023 was still less than 2 months’ income, similar to what it was two decades earlier. It’s the only major Canadian city where home prices have not outpaced incomes, making it the most affordable urban centre by a wide margin.

In Calgary, housing affordability has slipped somewhat since 2019 but it remains the second-most affordable urban centre in Canada, and its edge over other markets has grown. What’s especially remarkable is that housing in Calgary remains relatively affordable despite record population growth over this period.

The minimum down payment in Calgary increased from just over two months of income in 2019 to about eight months in 2023. That’s a meaningful increase, but modest compared with Toronto and Vancouver, where buyers need additional years, not months, of income to purchase a home. Even Montreal, with a population growing at only a quarter of Calgary’s pace, has seen a larger deterioration in affordability.

What’s behind the divergence in housing affordability between Alberta and other provinces? For one, Alberta’s major cities have been able to build quickly and respond more effectively to population growth. According to the Canadian Home Builders’ Association benchmarking study, Edmonton scores first in its overall ranking on housing construction metrics, with approval timelines eight times faster than Toronto, as well as significantly lower municipal fees — less than a fifth of those in Toronto or Vancouver. Calgary also performs well overall, ranking fifth out of 23 cities, well ahead of Vancouver and Toronto, which rank 17th and 21st, respectively.

Edmonton and Calgary also benefit from greater supply of developable land, enabling housing construction to respond more easily to a growing population. This will likely have served them well since 2023 (most recent data) as they continued to experience record population growth.

Relative to other provinces’ major cities, Alberta has never had as wide an advantage in housing affordability as it has most recently, even after absorbing significant population growth. That advantage is likely to continue attracting migration to the province, particularly young families seeking the detached, single-family homes that seem unattainable in other cities.

Have an idea for our next EconMinute? Email us at media@businesscouncilab.com.